Why Libra makes me even more bullish about Bitcoin

This post was originally written on June 19th, 2019 on Medium

On June 18, 2019 Facebook finally unveiled Libra their cryptocurrency project to the world.

The announcement has drawn the attention of the entire cryptocurrency industry, media, technology industry, and even public markets. After diving into the technical whitepaper and talking to industry insiders. My conclusion is — While Libra itself is not that interesting, it makes me even more bullish on Bitcoin than ever.

In this tweetstorm turned blogpost I want to lay out the reasoning on why I think this is the case. Keeping in mind Libra is not officially being launched until 2020 so many of these assumptions can change between here and then.

The bull case for Libra (& Crypto at large)

Before laying out why Libra is not very interesting, I do want to highlight a couple of the more interesting aspects of the project.

Cryptocurrencies are serious business

One of the largest internet companies in the world is launching their own cryptocurrency and their own blockchain is a huge validation point for everyone. Back in 2013 when I first started in this space, this fact would have been unimaginable.

David Marcus and team are real operators with real experience scaling large companies. Facebook is bringing their A team to the cryptocurrency market, this isn’t some small innovation team experiment for them.

Basket of fiat outside of USD

Libra is not just a fiat-pegged currency but rather a basket of fiat currencies. Facebook wants to create a global currency rather than just a USD replacement.

The Libra project is essentially a programmable stablecoin that is backed by a basket of fiat currencies & governed by all of its members. If Facebook keeps their promise to not control more than 1% of the network, it could be a real alternative rail for some types of payments.

Largest potential on/off ramp

The crypto market has an estimated 30M-40M users today (a projection from my post last year) and Libra has the potential to onboard 2B more people into this market. That’s a huge step function increase and cannot be ignored.

If correctly executed, Libra could become the largest on/off ramp for the crypto industry by orders of magnitude. This is also a critical part of the financial infrastructure stack to help enable all other types of crypto applications as well (remittances, B2B payments, etc.).

Identity, KYC, and AML built in

As CZ, the founder of Binance, puts it best, Facebook already has all of your identity info for KYC so users won’t need to input any other data.

On a more serious note if this could be packaged up and portable, this would solve so many of the identity issues in the crypto space and help the industry as a whole move towards a much more compliant future.

There are some major privacy implications of this, which cannot be ignored, which we’ll get into later in this post.

The bear case for Libra

No community or ecosystem

Before they have even launched Libra has already alienated many developers in the crypto ecosystem and much of the top advocates in the industry. The majority of the people who have been building products and services in this ecosystem are not excited about Libra. We did an informal poll at our crypto event yesterday and not one developer was excited about Libra’s release.

On top of this Facebook has a consistent track record of treating its developers unfairly, changing rules on its platform, building their own competing projects to compete with developers, etc.

Existing crypto users won’t use it

Arguably the dominant use-cases in the crypto space today are: exchanges, mining, trading, and store of wealth. For all of these existing users who use crypto extensively today, I do not see them switching over to Libra for the overwhelming majority of use-cases.

There is no way someone storing their wealth in Bitcoin (non-sovereign, censorship resistant, unseizable asset) would ever move their assets over to Libra. To help illustrate this point here is a comparison chart of Bitcoin, Libra, and some of the other major cryptocurrencies.

Targeting the wrong customer segment

Given the two points above, Libra is fundamentally betting their distribution advantage will help them win a whole new segment of users (more “normal” users) for new use-cases (remittances, etc).

Given Libra is backed by a basket of fiat currencies, you are in essence giving up the upside of investment while subject yourself to volatility (FX & exchange risk). People will never 10x their money by buying Libra so at most it can only be a valuable bridge currency.

Comparison chart of USD, EUR, GPB, AUD, NZD

Emerging countries have many other market dynamics

Given most people in developed countries would not convert their fiat currencies to Libra, they would mainly be targeting emerging countries.

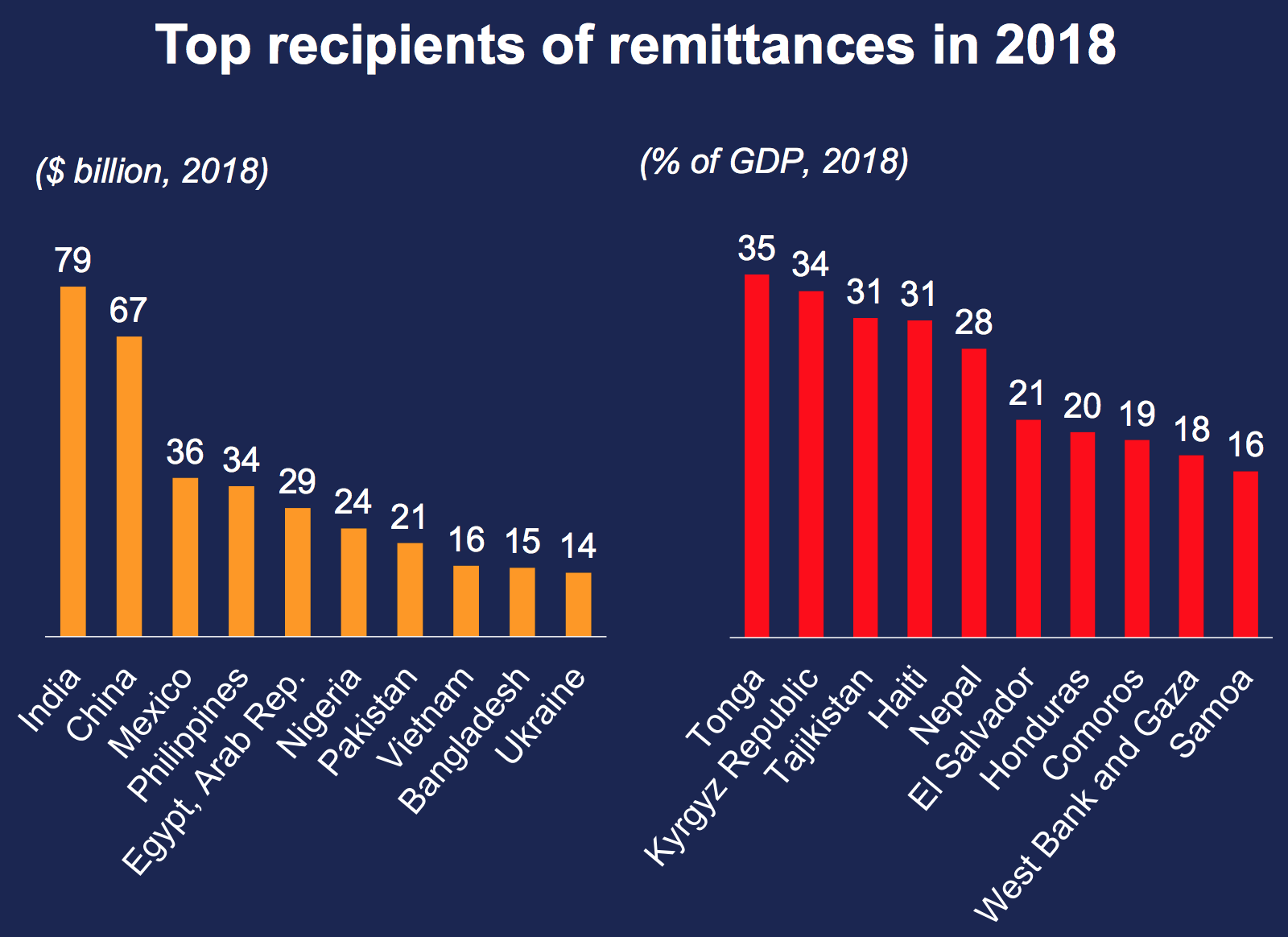

Along with Facebook’s big vision to “bank to unbanked” one of the main markets Libra is touted to be going after is the remittance market. While in theory this is a large ($550B) and underserved market I’ve looked deeply into the remittance market and I do not see Libra playing much of a role here. The reality of remittances is — 80% of the worldwide remittance volume is handled via cash payments which requires money transfer operators (MTO) to have both physical presences & cash inventories.

While in theory Libra can partner with organizations to facilitate these cash transactions, nothing in their announcement shed any real details on how they would approach this. Crypto companies as a whole have not reached any significant volume in the remittance market.

On top of all of this, crypto is banned in India & China. Given Libra would have to comply with local regulations which cuts out 2.7B of their target demographic.

Regulatory risks for Libra

Facebook itself is already a very unloved company (it has an NPS score of -19, which is lower than all of the banks), is facing multiple lawsuits, is at the center of major privacy violations, and is in the political hot seat for its role in influencing elections around the world.

I forecasted that there would be no way Facebook would be able to launch their cryptocurrency initiative quickly, and already we are starting to see international and domestic politicians react to their announcement.

Moving fast and breaking things might have worked when Facebook was starting up, but I do not believe they will be able to take this same approach if they are trying to move into core banking/money services.

I predict that Libra will have to delay their 2020 launch date, not for technical reasons, but rather political and regulatory reasons.

Why Libra makes me even more bullish about Bitcoin

My personal takeaway is Libra at best will be a core fiat gateway for Bitcoin, and at worst case will be a closed & permissioned network that violates the privacy of its users to an even greater extent.

On the other hand, Bitcoin is aiming to become a worldwide store of value asset. Bitcoin is also moving towards this goal without a billion dollar company behind it, without the need of member organizations, without a leader, and without a large existing install base.

It is achieving all this purely through the incentive structure of Bitcoin itself and forming a large international ecosystem behind it. To me Bitcoin is far more revolutionary in its intent and is addressing a much larger total addressable market and for those reasons Libra makes me even more excited about Bitcoin.